Company of the Week

At Sequoia, we frequently have a company of the week case study. The exercise usually starts by showing some financial information about a company and having everyone guess what the company is or some other facts about the company. There is always some story or point behind the exercise that we reveal afterwards.

Here is what I sent to Team Sequoia yesterday.

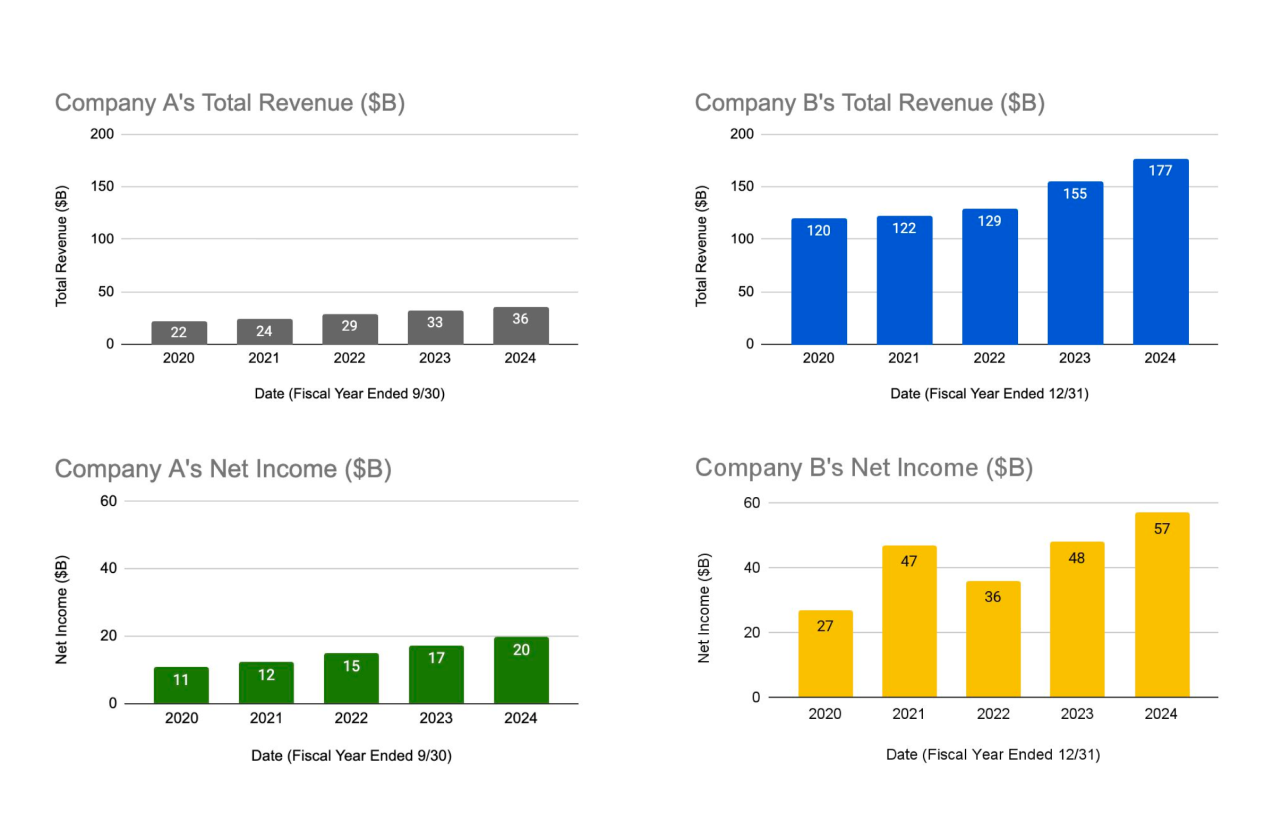

Company A and Company B’s revenue and net income. Both company A and company B are in the same industry.

- What is company A?

- What is company B?

- What is the ratio of valuation of Company A to Company B?

Scroll for answer

The answers for the “Company of the Week” exercise are:

- Company A = Visa (NYSE:V)

- Company B = JPMorgan Chase (NYSE:JPM)

- V and JPM’s market capitalizations are about the same.

Visa is one of the world’s leaders in digital payments and facilitates worldwide commerce and money movement across more than 200 countries and territories among a global set of consumers, merchants, financial institutions, and government entities through innovative technologies.

JPMorgan Chase is a multinational financial services created in 2000 by the merger of J.P. Morgan & Co. and Chase Manhattan Company. It is the largest bank in the United States and the world’s largest bank by market capitalization. The firm is the world’s fifth-largest bank by total assets and the largest investment bank by revenue. The company’s fortress balance sheet, geographic footprint, and thought leadership have yielded a substantial market share in banking and high brand loyalty.

Both are fabulous businesses, but the market rewards business quality. V has beautiful network effects with a less capital-intensive business with much more predictable revenue, a much higher profit margin, and a less cyclical business than banking.

There are a few reasons for constructing this exercise:

- I attended JPM’s Tech 100 conference this week. Those who checked my calendar or bumped into me at the conference had an advantage in figuring out this exercise. One of the bankers at JPM introduced me to an executive at V and reminisced about working on V’s IPO, but now they have the same market cap.

- This week, I debated with a few founders who wanted to apply some other company’s valuation multiples to their company to determine their valuation. Here is an excellent example of how the market values revenue and net income from different companies sometimes extremely differently. JPM’s net income is greater than V’s revenue, yet the two companies’ market cap is the same. That’s wild!

- At recent board meetings, we discussed the importance of the quality and predictability of revenue and profits. There was a time when we used ARR strictly for annual RECURRING revenue. Somehow, it has become bastardized into annual revenue run rate, regardless of whether the revenue is recurring or not. It started by run-rating quarterly numbers but then twisted into run-rating monthly and even weekly numbers. Heck, why stop there? One may be able to fool some people in the short term, but the market rewards high-quality business in the long run.

- When we create “Company of the Week” exercises, we try to stump Andrew Reed, who has an encyclopedic knowledge of public company financials. Indeed, he answered correctly before everyone else, but I wanted to create an exercise many could figure out. Focusing on Company B, how many companies could have generated $177B in revenue in 2024? Then, you can go from there. Or focusing on Company A, how many companies have consistent >50% net income margins. Many of you broke down the problem into smaller problems and got the correct answers, too. Well done!

- Recently, a prominent university dean disclosed that half of the faculty still do not use ChatGPT, Grok, Claude, or Perplexity and have not changed their pedagogical approach to LLMs. I was shocked! Computers are so good at reverse look-up, so this exercise should be easy for LLMs. Who wouldn’t want to remember financial facts better than Andrew Reed? It turned out that using LLMs was not universally helpful to all. Some found the answer in one shot using o1 and deep research. Others got it after a fair amount of prompting. Some never found the answers using their favorite tool. Even after LLMs find the answers, interpreting the results requires human thought, at least for now.

Moral of the story: (1) business quality matters, (2) pay for and use the best LLM tools, and (3) use the rest of the time to think and puzzle through what LLMs cannot.